Investment Advice from the Great Depression: Buy Low!

In the spring of 2020, as the bottom was falling out of the markets during the Covid-induced crash, one of my partners, Michelle Damon, CFP®, shared a fascinating historical document. It was a well-worn copy of a type-written letter that Dean Witter, founder the large eponymous brokerage firm (which has since merged with Morgan Stanley), shared with his company in 1932 at the market’s rock-bottom and from the depths of The Great Depression’s despair.

What was Witter’s message? The full memo is copied below, but, in summary, here are a few key comments:

“History tells us that this is not the first time we have had major economic problems, and it is possible that things could get worse. But just as surely as conditions righted themselves before—gradually readjusting to normal — so they will again. The only uncertainty is when.”

“The current market offers the buyer a splendid opportunity. I dare say that great fortunes will be made out of securities bought today.”

“This is the time to use the dollar to buy good securities, whether greatly depreciated bonds or excessively deflated common stocks… Why not invest it now, when securities are cheap?”

How did Witter’s Advice Hold Up?

The stock market hit rock bottom on July 8, 1932, two months after Witter’s letter, and down 89% from the previous market peak in 1929!

Despite the hardships of the depression-stricken 1930s, stocks did begin to climb from that point. The month of July 1932 alone saw a 51% climb in the S&P 500 index!

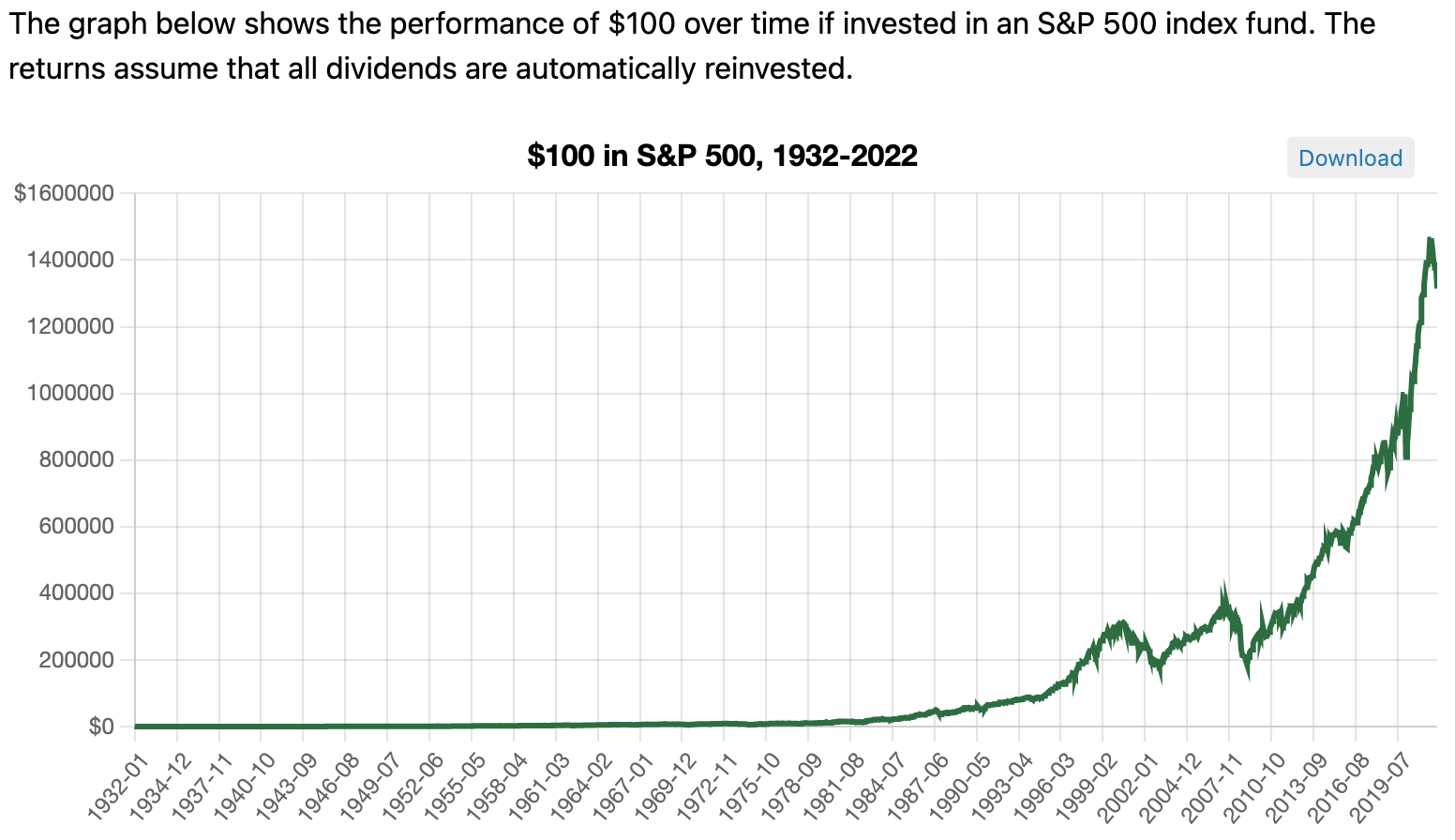

While many individual companies have come and gone over time, for broadly diversified investors, the climb was staggering. Here’s an inspiring site illustrating the value of $100 invested in 1932 throughout the following years. While the growth on this chart is nearly unnoticeable from 1932 to 1982 due to the scale of the chart, if you use the slider on the chart (click through to the website to use the slider), you can see the impressive growth in dollars before the vertical climb really begins!

Dean Witter’s 1932 Memo to Investors

A very interesting book could be written on mass psychology and the effects thereof. That everyone is influenced more or less by the opinion of others is obvious. There was no reason for the unwarranted heights which the markets reached in 1929 except universal over-optimism—there is no excuse for the present market value of good bonds and stocks today except undue pessimism. In 1929 no pessimistic comment could survive. Today an expression for confidence in the future of the country is unpopular. Strangely, the peaks of 1929 and the low quotations of today are both due to the same cause, which is lack of intelligent and sound analysis. It is strange that such divergent conditions should come within such a short period and should be due to such identical factors.

We are no longer much interested in the fantastic heights of 1929 except that we marvel at our lack of sane judgment. We are keenly interested in the present, and until some time elapses and we can obtain a better perspective it is difficult to realize that present conditions and markets are just as abnormally low as 1929 conditions and markets were excessively high.

There are only two premises which are tenable as to the future. Either we are going to have either chaos or else recovery. The former theory is foolish. If chaos ensues nothing will maintain value, neither bonds nor stocks nor bank deposits nor gold will remain valuable. Real estate will be a worthless asset because titles will be insecure. No policy can be based upon this impossible contingency. Policy must therefore be predicated upon the theory of recovery. The present is not the first depression; it may be the worst, but just as surely as conditions have righted themselves in the past and have gradually been readjusted to normal so this will again occur. The only uncertainty is when it will occur.

Everyone now seems to be indulging in the futile desire to buy at the bottom, just as everyone sought the very top in 1929. Most conservative people thought that values were much too high in 1928. Their judgment has since been fully vindicated in spite of the fact that values went much higher in 1929. Someone once said that they had made their fortune because they had never tried to buy at the bottom or selling at the top. This only means that they had not striven for the impossible but had been satisfied to buy when values were in general low and had been satisfied to sell when values were in general high, and without regard to peaks, which no one can identify and which, except by accident, are impossible to attain.

I think everyone must know that values are abnormally low. In a few years and with a better perspective they will realize that they were low in 1931. In other words, they were even then way below normal. People are deterred from buying good stocks and bonds now only because of an unwarranted terror. Almost everyone says that prices are going still lower. All sorts of bugaboos are paraded to destroy the last vestige of confidence. Stories of disaster which are incredible and untrue are told to foolish and credulous listeners, who appear willing to believe the worst.

I wish to say definitely that values were low in the latter half of 1931 and that they are now ridiculous. To prove this one has only to take an average period of 10 to 20 years of earnings, which should provide proper normal, and compare present values with the value which such normal earning power would adequately support. The stocks of many good companies which are faced with no ascertainable financial hazard are selling at only 2 or 3 times 10 year earnings, and at from 5% to 50% of sound book value, disregarding such valuable intangibles as good will, going concern value and trained intelligent organizations which it has taken years and the expenditure of vast sums of money to develop. I wish to say emphatically that in a few years present prices will appear as ridiculously low as 1929 values already appear fantastically high.

In 1929 one could only profit by selling. Many of us are instinctively reluctant to sell. There was the problem of reinvestment—there were taxes to be paid on profits. Today the situation is reversed. The present offers a splendid opportunity to the buyer. Great fortunes will be made out of securities bought today. There is no tax on buying and there is no sentimental deterrent. Only unwarranted fear or a futile desire to buy at the very bottom deters people from investment now. Most people who are buying at all are buying Treasury Certificates or the highest grade of municipals. Some are even putting money in their safe deposit boxes. None of these things are cheap. By comparison they are most expensive.

The time to have bought Treasury Certificates and the highest grade of short term obligations was in 1928 and 1929 when values were high and in order to preserve the dollar intact. The present is the time to use the dollar in the purchase of good securities, whether they be greatly depreciated bonds or excessively deflated common stocks. All of our customers with money must some day put it to work —into some revenue‐producing investment. Why not invest it now, when securities are cheap? Why leave it in cash or invest in Treasury Certificates which are dear? Some people say they wish to await a clearer view of the future. When the future is again clear the present bargains will no longer be available. Does anyone think that the present prices will continue when confidence has been fully restored? Such bargains exist only because of terror and distress. When the future is assured the dollar will long since have ceased to have its present buying power. If one holds either cash or the very highest grade of short term bonds as a temporary medium of investment he will find that he has only permitted great investment opportunities in tremendously underpriced securities to escape him.

It requires courage to be optimistic as to the future of the country when nearly everyone is pessimistic. It is, however, cowardly to assume that the future of the country is in peril.

No successful policy can be established upon this unsound theory. It is easy to run with the crowd. The path of least resistance is to join in the wailings that are now so popular. The constructive policy, however, is to maintain your courage and your optimism, to have faith in the ultimate future of your country and to proclaim your faith and to recommend the purchase of good bonds and good stocks, which are inordinately depreciated. You will gain the respect of those people with whom you come in contact by such an attitude. If you can persuade them to evidence their confidence in the future of the country by the purchase of good securities now you will do them a great favor and they will be grateful to you later.

It is disconcerting to have recommended the purchase of securities in 1931 as they have gone much lower since. This shakes one’s confidence in his own judgment. You were just as right, however, in 1931 as you are now in recommending investment in securities which were even then cheap. I can remember distinctly that I could find no justification for values which existed in 1928 and in many cases recommended sale or advised against purchase. I was decidedly wrong, as prices went much higher in 1929. I was only wrong, however, in that I failed to pick the very top of the market. It is true that values in 1928 were already inordinately high as judged by normal and average yardsticks.

On April 18, 1929, I dictated a memorandum which was published to the entire organization, copies of which are still available in the files. The subject matter of the memorandum was unpopular. It stated that people were buying stocks without regard to “value, earning power and dividends, present and prospective.” It stated that people were buying stocks not because they were worth the price at which they were selling, but because they hoped they would go higher and could be sold at a profit. The memorandum stated that the average speculator who bought stocks upon that theory in the long run lost money. It compared the psychology which then existed (April, 1929) with the psychology of the Florida land boom, the commodity inflation of 1919 and other characteristic periods of inflation. It pointed out that one could not afford to buy stocks that earned less than 5% and paid less than 3% on market values then prevailing. It stated that “perhaps we are going to have the greatest era of prosperity in our history.”

“Maybe we have already had this era. Perhaps we have nothing but increasing earnings and increasing dividends ahead of us. I hope so. If we have, present values are hardly justified; if we haven’t they will decline. Many things can happen, most of them unforeseen—politics, wars, economic changes, European competition, money shortage, withdrawal of foreign balances, adverse foreign trade balances, sudden withdrawal of large sums of bootleg money in the call market, Federal Reserve restrictions, interference by Congress or by the Government. These things probably won’t happen but might. If they don’t present levels may be all right—if they do, the last holder will suffer and not the next to the last, but we can’t all be next to the last.”

“The danger signals are waving—higher time money than we have ever known—more speculation than ever before, and tremendous brokers’ loans, though this may be a proper and normal increase in a very rapidly growing country. Not only are the rich and intelligent speculating but many have “their last dollar in the stock market on margin. $5,500,000,000 of record and a great deal more, unrecorded, is borrowed to carry stocks. People are paying 8% or 9% for this money and generally getting 3% or 4%. How long can this last? Can it last until the 3% or 4% catches up to the 8%? Probably not.”

“I am not a stock market prognosticator nor an analyst. I do not pretend to be a Moody, a Babson, or a Brookmire. I have been rather pessimistic about stock market prices for two years. If I had been an unqualified optimist I could have made a great fortune. I am not a pessimist—I think this country will prosper beyond conception in the next 20 years. I don’t, however, believe in over-speculation. I don’t believe in 9% money for 3% stocks. The former may be temporary—the latter is more or less permanent unless price levels change. I have been taught that a good stock should earn 10%, not 5%. Probably I am old-fashioned. In any event, this is not the prevailing custom today. I believe that people should speak honestly and not too guardedly. I would not want our brokerage department to be the means or vehicle of severe loss to people. It is hard to be patient with 3% stocks carried on 9% money. Will they stay at a level which produces a 3% return? John Moody and a great many other excellent authorities seem to think so. I don’t know but I would not gamble on it.”